People in the TV channels, discussion forums and every media platform will drive your emotions to buy or sell a particular stock using their influence.

Many retail traders and investors have thirst of making money. Their emotions carry them. They take positions based on the media, then the real game begins. Big players will start exiting from that stock by trapping retailers at higher levels.

No one will know the reality until experience teach you with a tight slap.

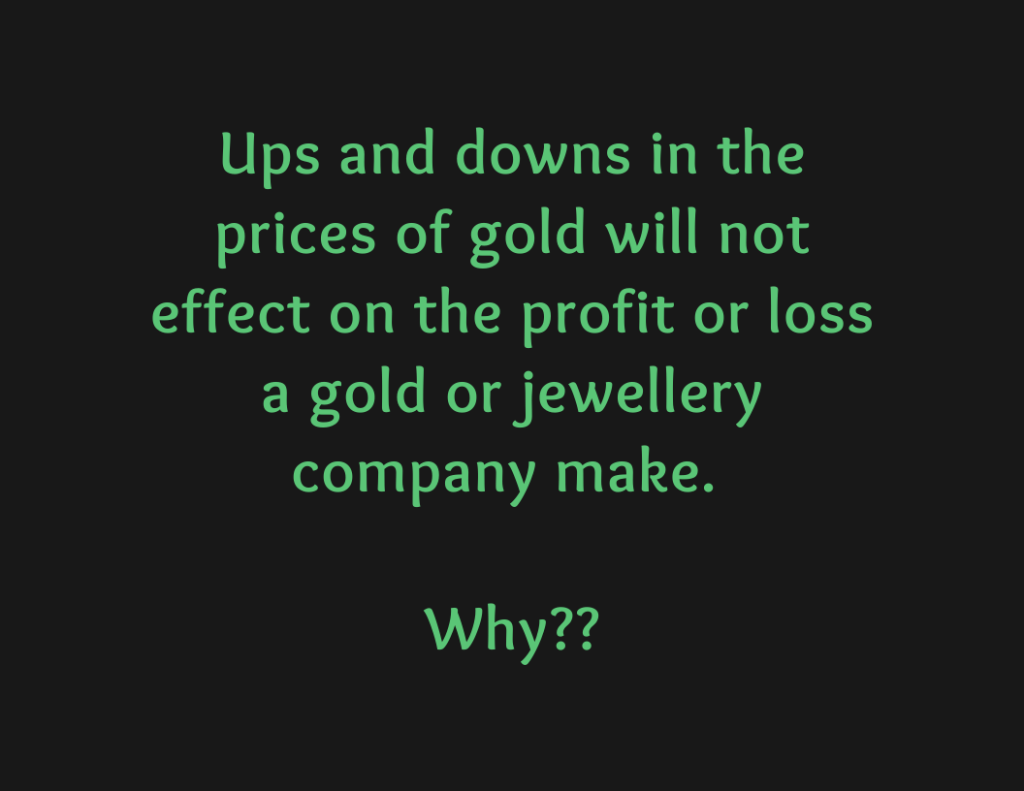

Daily movements of the gold prices will not have effect on the companies which depend on gold like Titan Jewelers, Kalyan Jewelers. Let’s see why?

See the other side of coin for better understanding, for instance, if the gold prices fall sharply from here, will the jewelry companies get loss? No. If it is the case, they cannot run their business. Companies will follow hedging mechanism to avoid the impact of daily fluctuations.

Hedging is the process of taking counter position in the future segment to avoid loss. In this context, if Kalyan Jewelers bought 100 Kg of gold for manufacturing new ornaments, it will sell the same amount of future trading contracts in the share market to hedge their investment (Futures and options are the derivatives which are introduced for hedging). So, for every 1 rupee increase in the price, they will get profit in their asset which they bought and at the same time loss in their position which the company shorted.

Then, you may get a doubt, “How do gold companies make money?” Through making charges, they will make money and there are several other ways, we are not diving into that topic now.

Earning money will not make you rich. Yes, you heard it right. Only managing money smartly with that earnings will differentiate you from rest of the crowd.

We are already paying hefty direct and indirect taxes for the government and spending the remaining money for personal interests. Many people stick that left over pennies in the bank, may be in a fixed deposit mode. Come out of that web, amount just beats inflation at the end of the day. We also need to pay capital gain or capital appreciation tax. Then what’s the best thing to do ??

Many analysts will say that investing in the world of stock market will be profitable. Money will double in FD over a period of 10 years. Don’t aim 10 or 20 times return in the stock market by holding shares. Everyone is not Warren Buffet. Even the index did not give that much return. Current Nifty Index is at 15,000, before 10 years, it was roughly around 5,500. Yes, we got 3 times return in 10 years but what about the risk factor? Is it a worthy bet in terms of risk adjusted return? Index made our money double from the corona crash to this point of time. It’s the matter of taking right entry and right exit along with correct division of capital.

Ways to earn money from savings through an investment vehicle:

The list goes on. There are ‘n’ number of ways through which one can make money according to the risk appetite.

In my personal opinion, don’t boggle your heads by thinking where to invest for your future. Invest 20% to 30% of your money in mutual funds and debt instruments if you want that money to be safe by beating the inflation. With the rest of money, enter into stock market (secondary market). One can easily make more money and better than mutual fund returns if the right knowledge and analysis is with you. Getting 5% return in a month through short term is not a big deal !!

Learn the basics, observe the market for couple of months with back-testing, entering into short term investments. I don’t believe in long term investment and intraday trading. Both of that two requires a skill. With some knowledge and analysis, one can start in short term investments. Don’t jump in to open the demat account to invest right know. Learn first, earn next.

There comes a time in our life when knowing about money becomes a necessity rather than the option. Everyone is not from the finance background right. No worries, you are at the right place to understand things in a crystal-clear manner…

If we need some money to buy a new home or a vehicle, our eyes turn towards bank. What if banks need some money? Whom should they ask for? Will they come to you? Haha!! Certainly not. Banks will ask money from RBI. As we pay interest to the bank, banks pay interest to the RBI. That interest rate is known as repo rate. In order to maintain the inflation rate, RBI modifies the repo rate.

How much return you will get if you keep your money in the savings account? Hardly 3 to 4% depending on the bank. If interest rates are even more reduced like in USA, will people still save their money in banks? No. Money will flow into different asset classes.

Equities will increase when interest rates go down because money will flow into the riskier assets as they do not get much return from the fixed instruments. Anyway, government support via policies and liquidity must be there in order to push the market.

Gold is inversely related with the interest rates as per theory. When the interest rates go up, gold price has to come down and vice versa. Looking through practical lens, gold depends on various factors like International price, Rupee & US Dollar exchange rate and the last but not least is tax that government asks to pay. Gold is said to be safe heaven and people will rush to buy in panic. The best example is corona virus period graph uptick in the first few months. When everything becomes normal, then the prices stabilize.

Real-estate shoots up when interest rates come down and vice versa. It depends on various other factors like land value in that particular area, future growth of that specific town or city in which we are buying. Many big heads will turn their investments to real estate because only the registration cost and cost estimated according to the government will be paid as white money through transactions.

When everything doesn’t work, debt instruments will work. Debt instruments is good for short term duration if you ask me. For instance, if a person deploys his/her money in debt vehicles when the interest rate is lower. They have the risk of growing interest rate. Anyway, there are different types of debt instruments, we will discuss in the upcoming articles. There are many micro and macro-economic factors to consider before assuming the relationship between the financial instruments but everything comes under same umbrella i.e., rotation of money from one asset class to another asset class.